Zumper’s rent data provides insights to where the Consumer Price Index (CPI) is heading

Produced monthly by The Bureau of Labor Statistics (BLS), the Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for goods and services, including rent. Since the Cost of Shelter CPI uses existing paid rents, among other data points, as part of its calculation, there is a lagging nature to the CPI’s shelter cost component. Zumper’s data, however, serves as a leading indicator of shelter cost as we measure true market rents.

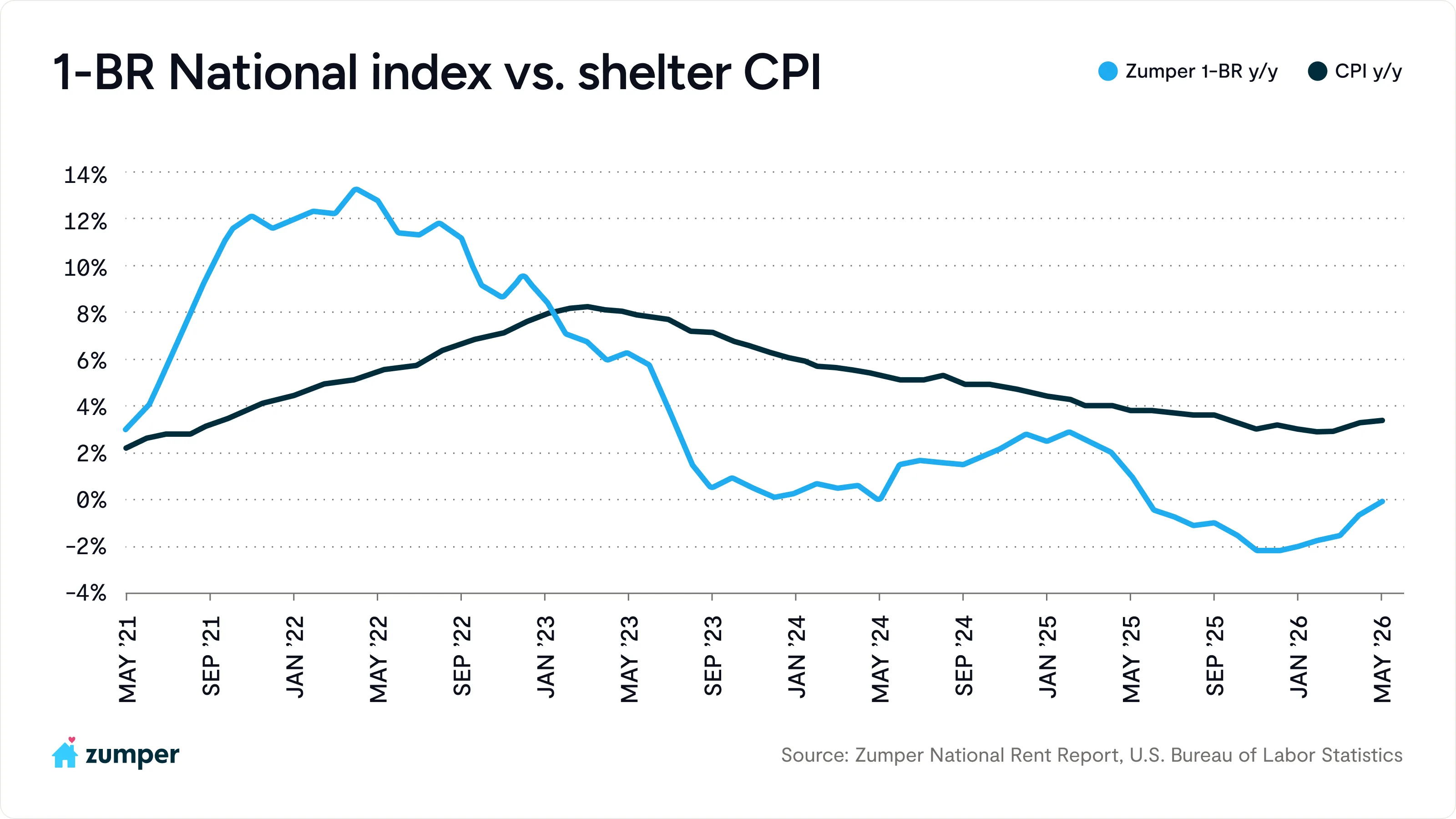

The May CPI report showed headline inflation over the trailing 12 months reaching 4.2%, the largest annual increase since April 2023. Meanwhile, the shelter index rose 0.3% in May, half of April’s pace, and on a year-over-year basis ticked up slightly to 3.4%, a modest acceleration from the 3.0% reading in March but roughly in line with April’s 3.3%. While shelter remains the single largest contributor to core CPI, the monthly deceleration is a welcome signal that the statistical distortions introduced by the federal government’s appropriations lapse in October 2025 are beginning to wash out of the data. April’s outsized shelter print was largely a methodological catch-up, and May’s more moderate reading supports that interpretation.

This is where Zumper’s forward-looking data becomes especially relevant. Our May National Rent Index continues to paint a picture that shelter CPI has yet to fully reflect. One-bedroom rents came in at -0.1% year-over-year, essentially flat, marking a milestone: the annual decline has now nearly closed entirely. May marks the fifth consecutive month of decelerating annual declines. Annual one-bedroom declines have narrowed every month since bottoming out at -2.2% last November, moving to -2% in January, -1.7% in February, -1.5% in March, and -0.6% in April before reaching essentially flat in May. National rents are now essentially the same price as they were a year ago.

The gap between what the shelter CPI is recording and what the market is actually doing remains a meaningful source of disinflationary pressure still in the pipeline for shelter CPI. As leases signed during the soft rental environment of late 2024 and early 2025 continue to cycle through the BLS’s rotating survey panel, that mechanical drag should persist into the second half of the year. The key question is whether the current rebound in asking rents will begin generating new upward pressure that offsets that pipeline relief, and May’s data suggests that pressure is building.

For the Fed, the May data does little to open the door to rate cuts in the near term. With headline inflation now at a three-year high of 4.2% and core inflation edging up to 2.9%, the burden of proof for easing remains high. The signal from Zumper’s data is that the prolonged period of rent softness that provided a disinflationary tailwind to shelter CPI is over. With market rents flat on a year-over-year basis and monthly momentum building into the peak leasing season, the pipeline of mechanical shelter disinflation will have diminishing new market softness to draw from. Any further pickup in asking rents from here would begin working against the Fed’s inflation timeline rather than helping it. With rate cut expectations having already been pushed well into the future, the trajectory of market rents this summer may be the single most important domestic variable for the inflation outlook.

Related content