Zumper’s rent data provides insights to where the Consumer Price Index (CPI) is heading

Produced monthly by The Bureau of Labor Statistics (BLS), the Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for goods and services, including rent. Since the Cost of Shelter CPI uses existing paid rents, among other data points, as part of its calculation, there is a lagging nature to the CPI’s shelter cost component. Zumper’s data, however, serves as a leading indicator of shelter cost as we measure true market rents.

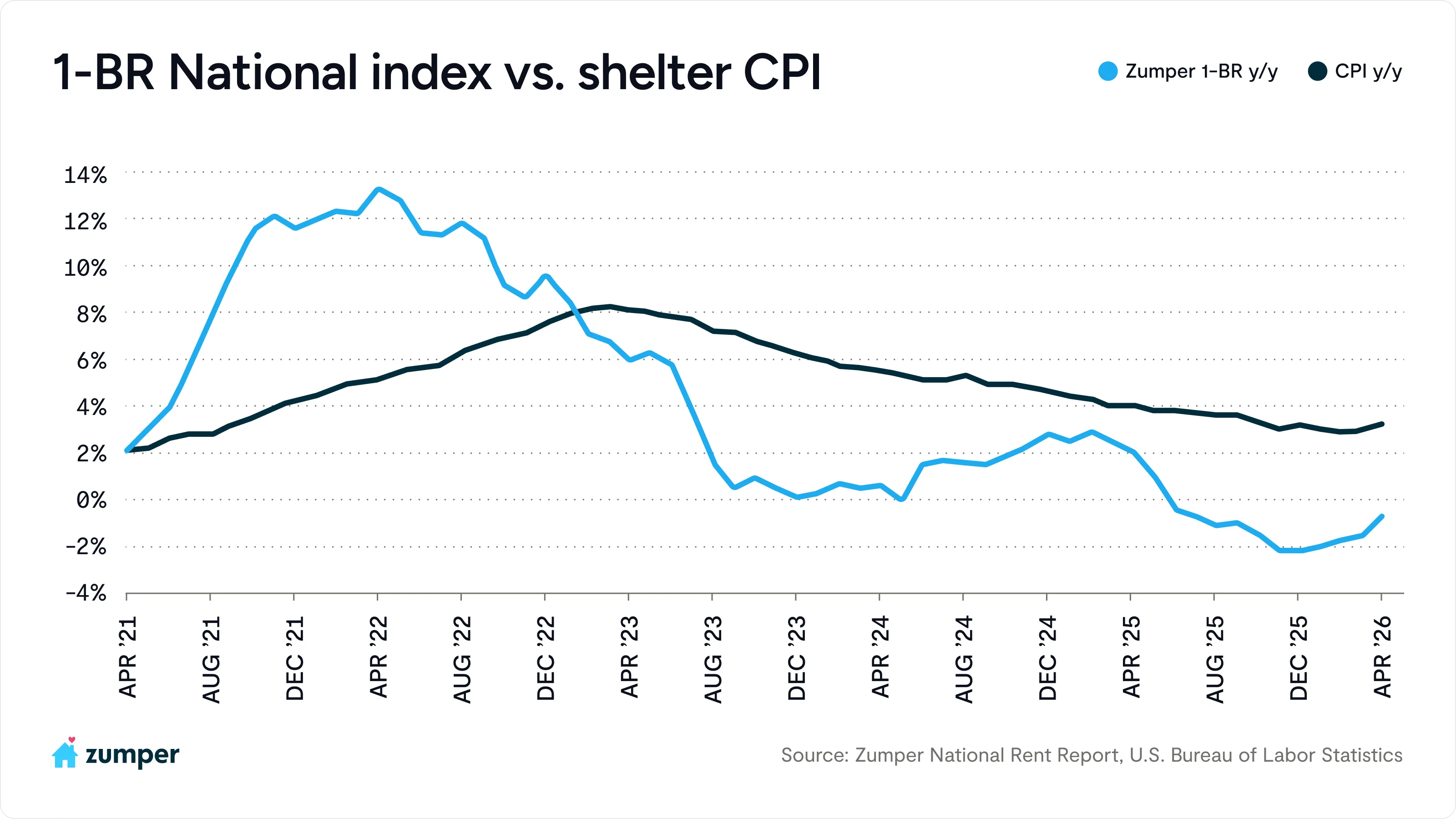

The April CPI report showed inflation cooling at the headline level month-over-month but accelerating on an annual basis. The all-items index rose 0.6% on a seasonally adjusted basis, a step down from March’s 0.9% gain, with energy once again the dominant force, rising 3.8% for the month and accounting for more than 40% of the headline increase as the gasoline index climbed 28.4% over the past year. Headline inflation over the trailing 12 months reached 3.8%, up from 3.3% in March and the highest annual reading since May 2023. Core inflation (all items less food and energy) rose 0.4% for the month and 2.8% over the year, the fastest monthly core pace since January 2025.

The shelter index rose 0.6% in April, double its March pace, and on a year-over-year basis ticked up to roughly 3.3% from 3.0% in March. But much of that monthly jump is a statistical artifact rather than a genuine market signal. When the federal government’s appropriations lapsed in October 2025, the BLS was unable to fully collect rent data and effectively recorded rental inflation at zero for that month. Because the BLS uses a rotating panel for its rent surveys, the next collection point for that sample landed six months later, in April, mechanically producing a sharper-than-usual catch-up in the shelter component. In other words, April’s shelter print reflects a methodological correction working through the data, not a fresh reacceleration in what landlords are actually charging.

This is where Zumper’s forward-looking data becomes especially relevant. Our April National Rent Index continues to point in the opposite direction of the headline shelter number. The standing gap between what the CPI is recording and what the market is actually doing remains a source of disinflationary pressure still working its way through shelter CPI, even as a one-off statistical reversal temporarily muddies the monthly reading.

With all of that in mind, the trend in our own data warrants a closer look. One-bedroom rents rose 0.4% in April to $1,508, the fourth consecutive monthly gain, and the annual decline narrowed sharply to -0.6% from -1.5% in March. That is the smallest year-over-year drop since the declines began and continues the pattern of decelerating annual softness we have flagged in recent reports. Some of that narrowing reflects an easier comparison against a soft April 2025 ($1,517), but the direction is consistent: the market is stabilizing and returning to more typical seasonal patterns after an unusually soft summer and fall. The story is no longer one of accelerating rent declines but one of declines fading toward flat.

For the Fed, the April data complicates an already delicate balancing act. The energy-driven strength may prove transitory, but with headline inflation now firmly above 3% for a second straight month and the gasoline shock tied to ongoing disruption in the Middle East, policymakers have limited cover to ease in the near term. The apparent core acceleration is softer than it looks once the shelter statistical reversal is stripped out, which the Fed is likely to see through. The more durable signal from Zumper’s data is that market rents have stopped falling and are flattening out. If that stabilization holds, the mechanical disinflation that shelter CPI still has to absorb would proceed without much help from new market softness, and any renewed upward pressure in rents would slow that process further. With the Fed’s latest projections already pointing to at most one cut in 2026, the flattening in market rents is the variable worth watching most closely in the months ahead.

Produced monthly by the The Bureau of Labor Statistics (BLS), the Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for goods and services, including rent. Since the Cost of Shelter CPI uses existing paid rents, among other data points, as part of its calculation, there is a lagging nature to the CPI’s shelter cost component. Zumper’s data, however, serves as a leading indicator of shelter cost as we measure true market rents.

The March CPI report delivered an inflation surprise, with the all-items index increasing 0.9% on a seasonally adjusted basis, which is well above February’s 0.3% gain, driven almost entirely by a historic 21.2% monthly surge in gasoline prices, the largest single-month increase since the series began in 1967. Headline inflation over the past 12 months climbed to 3.3%, up sharply from 2.4% in February. Core inflation (all items less food and energy) remained comparatively contained, rising just 0.2% for the month and 2.6% over the year, suggesting the March spike was largely energy-driven rather than a broad-based acceleration.

Within the core, shelter remained a persistent source of upward pressure, rising 0.3% in March and 3% year-over-year, still the single largest contributor to core CPI. This is where Zumper’s forward-looking data becomes especially relevant. The shelter CPI’s well-documented lag means it continues to reflect lease agreements signed months ago, not current market conditions. Zumper’s March National Rent Index tells a more nuanced story: annual rent declines are continuing, with one-bedroom rents down 1.5% year-over-year and two-bedrooms declining 1.3%. That gap between what the CPI is recording and what the market is actually doing represents meaningful disinflationary pressure still in the pipeline for shelter CPI in the months ahead.

However, with that said, the monthly picture warrants attention. One-bedroom rents rose 0.2% and two-bedrooms increased 0.1% in March, which is the first time both bedroom types have posted simultaneous monthly gains since May 2025, and the third consecutive month of decelerating annual declines. This points to a market gradually stabilizing and returning to more typical seasonal patterns after an unusually soft summer and fall.

For the Fed, the March CPI data complicates an already delicate balancing act. The energy-driven spike may be transitory, but with headline inflation back above 3% and the shelter component still elevated, policymakers have limited cover to ease policy in the near term. The Fed’s latest projections already pointed to just one rate cut in 2026, with meaningful odds of none at all. If Zumper’s data is right that shelter inflation has further room to fall mechanically, that could provide a disinflationary tailwind later in the year, but the stabilization in monthly rent trends is a variable worth monitoring closely. Any sustained renewal of upward rent pressure would slow that process and push the timeline for cuts even further out.

Contenu associé